A recent article in the Financial Times points to a structural shift underway in how audit oversight is evolving in the United States.

As quoted in the article:

“Focusing inspections on quality control systems rather than individual audits would shift accountability to the leadership of the firm and their systems and processes.”

This single sentence captures a meaningful change in how audit quality is being evaluated.

From File Reviews to Firm-Wide Accountability

For decades, audit oversight has relied heavily on reviewing individual engagements after the work was completed. Inspectors selected files, examined workpapers, and identified deficiencies on a case-by-case basis.

That model does not scale.

Regulators are now signaling a move away from isolated file reviews and toward evaluating how audit firms operate at a system level: how quality is controlled, how risk is managed, and how consistency is maintained across the entire practice.

This is not lighter regulation.

It is a different regulatory model.

Accountability is shifting upward: from individual engagement teams to firm leadership, and to the systems and processes that run the audit.

Why Software Is No Longer Optional

Once oversight moves to the firm-wide level, the discussion fundamentally changes.

The question is no longer whether accounting firms will use software.

The real question becomes:

Which systems are accurate, reliable, and defensible enough to serve as audit infrastructure?

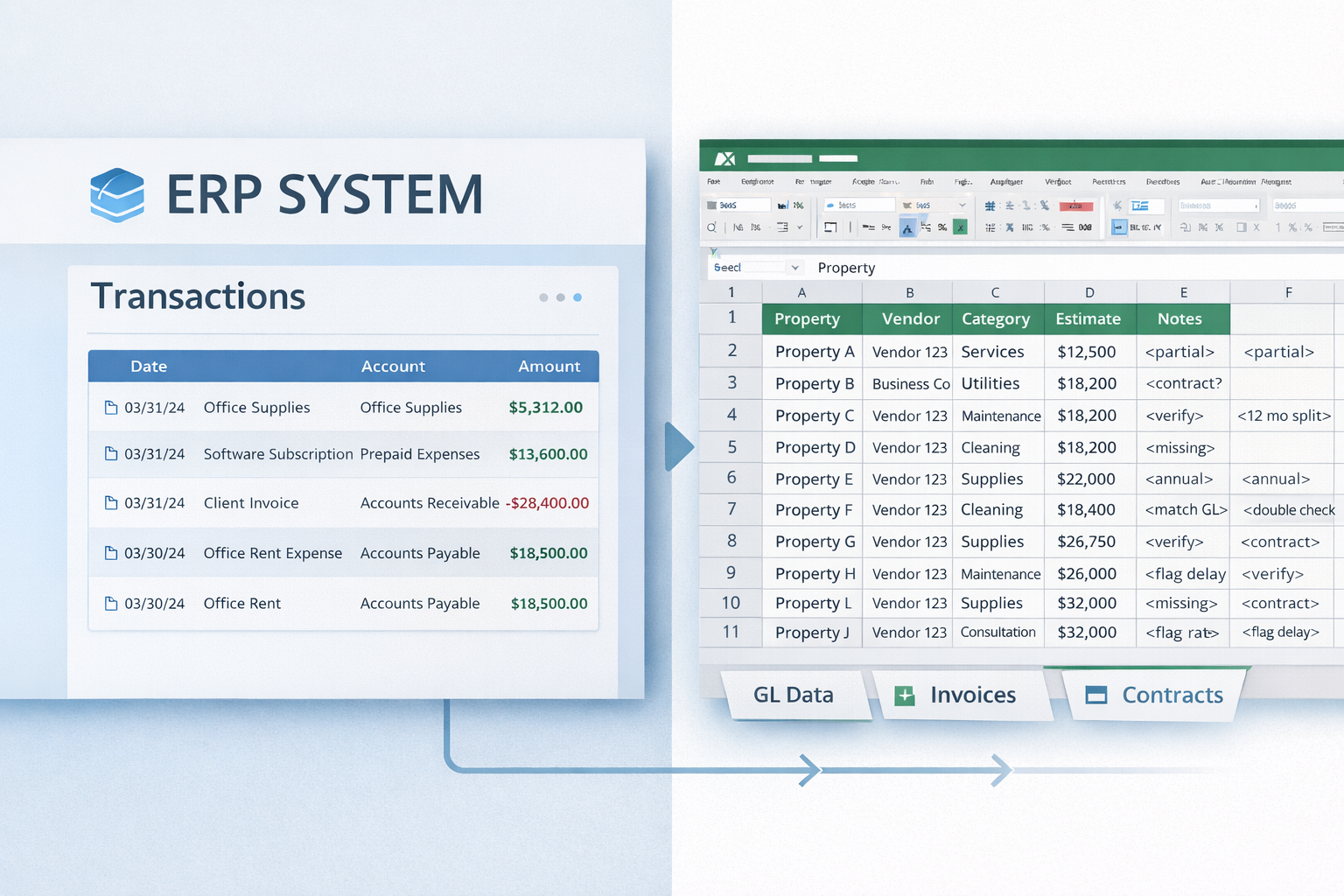

Manual workpapers, spreadsheets, and disconnected tools were built for a world of spot checks and retrospective reviews. They were never designed to support continuous visibility, consistent execution, or leadership-level accountability across dozens or hundreds of engagements.

Under system-level scrutiny, those limitations become impossible to ignore.

Building Audit Infrastructure, Not Just Tools

This shift is exactly why Verfi was built.

Not just an efficiency tool.

Not just an add-on to existing workpapers.

But audit infrastructure designed to support firm-wide control, transparency, and accountability.

As audit oversight evolves, firms will increasingly be measured not only by the outcome of individual engagements, but by the reliability of the systems they use to execute audits at scale.

A Structural Shift, Not an Incremental One

Audit is entering a structural transition.

The real choice facing firms is no longer whether to adopt software, but which systems they can actually trust to operate audits in a world where quality is assessed at the organizational level.

This shift will redefine how audit quality is demonstrated, defended, and sustained in the years ahead.